Innovations Beyond Traditional Finance: Exploring Next-Gen Solutions

In the realm of finance, a transformative shift is underway, propelled by the rapid pace of technological advancement. We find ourselves at the epicentre of a profound revolution, where age-old traditions collide with the limitless possibilities offered by cutting-edge technology, reshaping the very fabric of the financial sector. However, this digital transformation in financial services extends far beyond the aspects of algorithms and digital landscapes. It permeates every aspect of our lives, transforming our thinking, actions, and interactions.

At the forefront of this unstoppable wave of innovation, we witness the convergence of finance and groundbreaking technology like never before. WealthTech, FinTech, InsurTech, Suptech, and RegTech represent distinct yet interconnected domains within the financial technology ecosystem. Together, they fuel a disruptive force that transcends conventional boundaries, revolutionising how we manage wealth, access financial services, obtain insurance coverage, ensure regulatory compliance, and safeguard the integrity of financial systems.

In this blog, we embark on a journey to unravel the potential challenges associated with the seamless integration of these technologies. We delve into the key factors driving their adoption and explore how these advancements are revolutionising the financial landscape. Moreover, we witness the democratisation of access to financial services, the enhancement of customer experiences, and the empowerment of regulatory bodies to safeguard the integrity of financial systems.

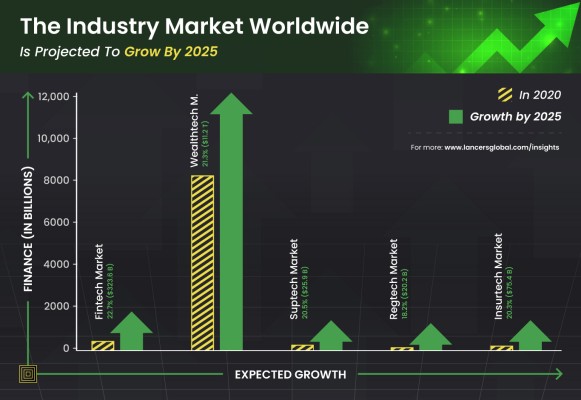

These statistics provide a glimpse into the future potential of these technologies. Now, let us embark on a comprehensive exploration, delving deep into their intricacies and understanding how they are propelling us towards transformative change.

What is Fintech?

Fintech is a rapidly growing industry that has the potential to revolutionise the financial industry. Fintech companies are using technology to provide new financial solutions and services that are more convenient, affordable, and efficient than traditional financial services. Fintech can also help improve financial inclusion by making financial services more accessible to people who are underserved by traditional financial institutions.

Factors Driving Adoption

- The rise of mobile devices: More and more people are using mobile devices to access the internet and financial services.

- The growing demand for convenience: People are increasingly looking for convenient and affordable financial services.

- The need for financial inclusion: Fintech can help improve financial inclusion by making financial services more accessible to people who are underserved by traditional financial institutions.

What is RegTech?

RegTech is an emerging technology that helps financial institutions and other regulated businesses improve their compliance with regulations. RegTech uses software, data analytics, and artificial intelligence to automate manual processes, identify risks, and improve compliance. As regulatory requirements continue to evolve, RegTech is likely to play an increasingly important role in helping businesses stay compliant.

Factors Driving Adoption

- Increased regulatory complexity: Regulatory requirements are becoming increasingly complex, which is making it more difficult for businesses to comply manually.

- Rise of FinTech: The rise of FinTech is creating new challenges for businesses, as FinTech companies are able to offer financial services that are not subject to the same regulations as traditional financial institutions.

- Advances in technology: Advances in technology, such as big data and AI in Regtech are making it possible to develop more effective solutions.

What is wealthtech?

Wealthtech is used to deliver financial services to high-net-worth individuals and families to manage their wealth. Adoption of wealth tech products directly helps automate investment management, provide financial planning tools, and offer other services to help wealthy individuals manage their money.

Factors driving adoption

- The rise of the millennial investor: Millennials are more likely to use technology than previous generations, and they are demanding more personalised and efficient financial services.

- The increasing complexity of the financial markets: The financial markets are becoming increasingly complex, and wealth managers need technology to help them stay ahead of the curve.

- The growing demand for transparency: Clients are demanding more transparency from their wealth managers, and wealthtech solutions can help provide this.

What is Suptech

Suptech is a promising new technology that has the potential to revolutionise financial regulation and improve supervision. It can help regulators improve efficiency, accuracy, and compliance, automate manual processes, identify risks, and reduce costs. As the financial markets continue to evolve, suptech solutions are likely to play an increasingly important role in financial regulation.

Factors Driving Adoption

- The increasing complexity of financial markets: The financial markets are becoming increasingly complex, making it more difficult for regulators to supervise them manually.

- The Rise of Fintech: Fintech companies are using technology to provide new financial products and services that are challenging traditional financial institutions. Regulators need to use technology to keep up with these changes.

- The need to reduce costs: Regulators are under pressure to reduce their costs. Suptech can help them do this by automating manual processes.

What is Insurtech?

Insurtech is bringing a shift in the way insurance is delivered. The Insurtech industry is using technology to improve customer service, reduce costs, and develop new products and services in the insurance sector. The adoption of Insurtech is being driven by a number of factors, including the rise of digital channels, the growth of data analytics, and the need for innovation.

Factors Driving Adoption

- The rise of digital channels: Consumers are increasingly using digital channels to shop for insurance. This creates an opportunity for Insurtech companies to provide insurance products and services through digital channels.

- The growth of data analytics: Data analytics is becoming increasingly important in the insurance industry. Insurtech companies can use data analytics to improve customer service, reduce costs, and develop new products and services.

- The need for innovation: The insurance industry is a mature industry, and there is a need for innovation. Insurtech companies can use technology to innovate and create new ways to deliver insurance.

Meeting Challenges Head-on with Innovative Solutions in the Financial Landscape

1. Regulatory Hurdles

One of the significant challenges in adopting Fintech, WealthTech, InsurTech, Suptech, and RegTech is navigating the complex regulatory landscape. As these technologies disrupt traditional financial services, regulators are grappling with adapting existing regulations or creating new ones to address the risks and opportunities they present. The lack of regulatory clarity and harmonisation across different jurisdictions can hinder adoption, as financial institutions are often cautious about compliance.

Solution: Collaboration between regulators, industry participants, and technology providers is crucial in establishing regulatory frameworks that strike a balance between innovation and consumer protection. Regular dialogue and engagement can help address regulatory challenges and promote the adoption of these technologies.

2. Legacy Systems and Infrastructure:

Financial institutions often face the challenge of integrating these tech solutions into their existing legacy systems. These systems, developed over decades, are built on complex architectures that can be rigid, siloed, and not easily adaptable to modern technologies. The integration process can be time-consuming, expensive, and prone to compatibility issues.

Solution: To address this challenge, financial institutions need to gradually invest in modernising their legacy systems. Adopting modular solutions, embracing open APIs, and using cloud-based technologies can facilitate seamless integration and interoperability with Fintech, WealthTech, InsurTech, Suptech, and RegTech platforms.

3. Data Security and Privacy:

As the adoption of financial technologies involves the exchange and storage of sensitive financial and personal data, ensuring robust data security and privacy becomes paramount. The risk of data breaches, cyberattacks, and unauthorised access is a significant concern for both financial institutions and their customers.

Solution: Financial institutions must prioritise cybersecurity measures and employ cutting-edge encryption techniques, multi-factor authentication, and regular security audits. Compliance with data protection regulations such as GDPR or CCPA is essential to building trust and ensuring customer confidence in these technologies.

4. Talent Acquisition and Upskilling:

The rapid advancements in Fintech and other technological sectors require a skilled workforce capable of leveraging and managing these technologies effectively. However, there is a shortage of professionals with the necessary expertise and experience in these specialised domains.

Solution: To overcome this challenge, financial institutions should focus on attracting top talent by offering competitive compensation packages, investing in training and upskilling programmes, and fostering a culture of innovation and continuous learning. Collaboration with academic institutions and technology providers can also help bridge the skills gap.

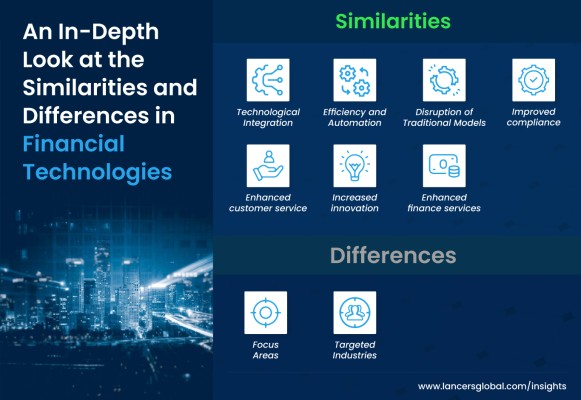

An In-Depth Look at the Similarities and Differences in Financial Technologies

Similarities:

- Technological Integration: All five domains share a common reliance on technology to drive innovation and transformation within the financial industry.

- Efficiency and Automation: Fintech, WealthTech, InsurTech, Suptech, and RegTech aim to automate processes, improve operational efficiency, and enhance customer experiences by leveraging technologies such as AI, data analytics, and automation.

- Disruption of Traditional Models: These domains challenge traditional financial models by offering alternative solutions, democratising access, and providing tailored services to customers.

- Improved compliance: Technology can help financial institutions track compliance data and identify potential compliance issues.

- Enhanced customer service: Technology can help financial institutions provide better customer service, such as by offering 24/7 support and personalised recommendations.

- Increased innovation: Technology can help financial institutions develop new products and services that meet the needs of customers.

- Enhanced finance services: All of these sub-industries are focused on using technology to improve the financial services industry.

Differences:

- Focus Areas: While Fintech encompasses a broad spectrum of financial services, WealthTech, InsurTech, Suptech, and RegTech have more specific focuses on wealth management, insurance, regulatory oversight, and compliance, respectively.

- Targeted Industries: Fintech has a wider application across various financial sectors, while WealthTech primarily targets wealth management and investment advisory services; InsurTech focuses on the insurance industry; and Suptech and RegTech cater to regulatory bodies and financial institutions.

Parting Words

The fintech, regtech, wealthtech, Insurtech, and suptech industries are still in their early stages, but they are growing rapidly. Their convergence is reshaping the financial industry. These dynamic domains represent distinct but interconnected realms within the financial technology ecosystem, driving innovation and transforming traditional financial processes. As these industries continue to develop, they are likely to have a major impact on services and create a more inclusive and efficient financial landscape.

Recent Posts

Add Comment

0 Comments